Keeping clear and accurate financial records is one of the basic tenets of running a business. Without them, you’re asking for trouble.

Investors, shareholders, and governments all want to make sure that the company is what it claims to be, does what it claims to do, and spends how it claims to spend. And the results if you fail to do this properly can be devastating to your business.

Audit time can be stressful and scary. And you’ll always be worried about little surprises hidden under a pile of papers. That is, unless you digitize and automate, and get ready for the eventual audit ahead of time.

As we’ll illustrate, audit preparation isn’t a last-minute job. In fact, you can stay ready for audit 24/7. With good transaction data captured automatically at the source, you barely have to lift a finger.

But we’ll get into all that shortly. Let’s start with the fundamentals.

The importance of financial auditing

To understand the values of a robust audit trail, you first need to remember why audits matter in the first place. An audit ensures that your financial statements are accurate, and that the company is spending money legally. Auditors go through a company’s bookkeeping ledger and match the transactions recorded against credit card statements or other financial documents.

While an audit can be done by anyone - you can audit your own finances, for example - we usually think of this process occurring in two specific cases:

You or your business is being audited by a government agency - the IRS (USA), or HMRC (UK), for instance - to ensure you’re following the law; or

Your business is being audited by a third party in preparation for a merger or acquisition

Both of these are mandatory in one way or another. If the government wants to audit your business, you don’t have a say in the matter. And if you’re trying to raise funds or have your company acquired, investors will want to make sure they’re getting what they’ve bargained for.

In either case, it’s vital that your financial statements are accurate. And to assess their accuracy, auditors will rely on supporting documents that you need to provide.

What is an audit trail?

A financial audit trail is a collection of documents or files that help to prove that financial records are accurate. Auditors work backwards from the financial statement to see every step that led to the final record - like tracing your path back using breadcrumbs.

Effective audit trails not only include documents themselves, but also track updates and alterations to records, and the people who made them. An audit trail wouldn’t work if it could simply be changed right before the audit takes place. (This would also likely be illegal, for what it’s worth.)

Of course, audit trails also exist outside financial record-keeping. For example, a computer log showing every login attempt counts. So does the ability to look back through the “version history” of a Word or Google document.

Finance teams need to provide the same possibilities when looking through a company’s records. You need to know who requests, approves, and executes each transaction, and you’ll need documentary evidence along the way.

Documents in an audit trail

So what kinds of documents make up an audit trail? Some of these are obvious, while others you may not have considered:

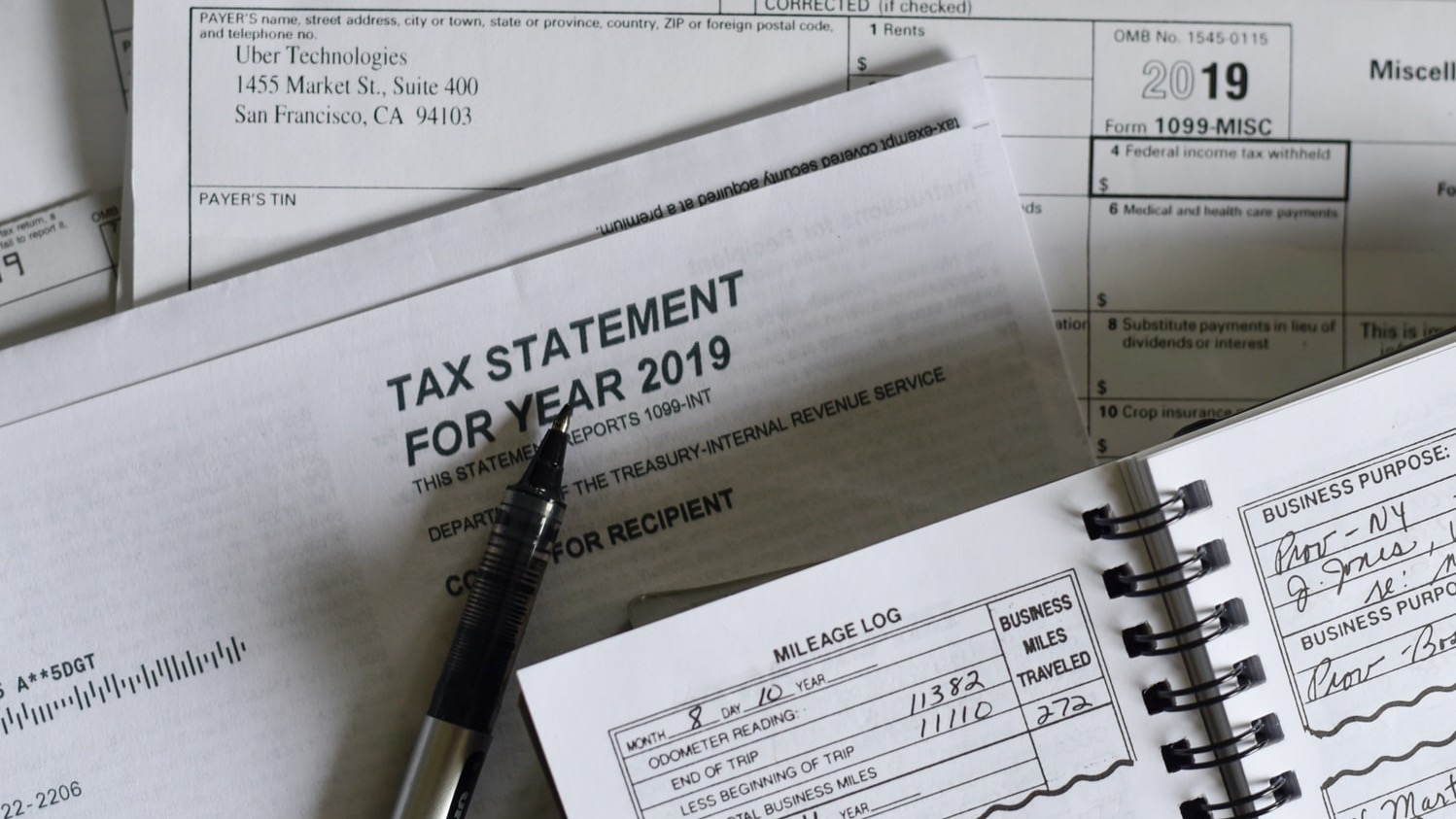

Receipts or invoices for every company transaction

Recorded approval for transactions, from a person with authority to give it

Change logs for any updates or alterations to purchase requests or approvals

Clear reasons given in any cases where the proper document can’t be provided

On top of simply possessing these documents, finance teams should ensure that they meet a certain level of authenticity.

Information that should be present on audit documents

Official financial records should of course live up to a particular standard. A receipt isn’t just any old scrap of paper, and purchase approvals also need to be recognizable as official.

The company - in line with local regulations - will decide its own standards. But typically official documents should have:

Time stamps to prove when they were created

A clear description of the transaction in question

An identifier for the person who made or approved the transaction

A record of any changes made to the document, with time stamps and identifiers to match

As technology advances, it’s becoming more important that these aspects occur automatically. Rather than a person verifying the time and place of an activity, it’s more reliable when done by computers.

As we’ll see shortly, an automated audit trail also saves time and energy, and ensures that you’ll be ready for any serious audit that approaches.

How to automate your financial audit trail

The financial audit trail revolves mainly around transactions: money coming into the company and purchases going out. So to automate the audit trail, you need solutions that digitize documents and capture key details at the point of payment. Otherwise, you’ll always have manual work to do.

Effective automation will target each of the key steps in the process.

Requests and approvals

Every company purchase requires some form of approval, even if the spender is pre-approved. This can occur before payment - as for purchase orders - or after the transaction - as we see with expense claims. But either way, someone with sufficient authority needs to approve.

Which in most companies happens by email or in writing, so you have a record.

But the best method is to require approval within the payment system itself. For example, suppose you use virtual credit cards for online purchases. When an employee wants to take a software subscription, they create a virtual card. But before the funds are “unlocked” for them, their manager needs to approve within the system.

The same works for corporate expense cards (they’re like company cards, but safer), and for digitized expense reports. An employee requests funds (or a reimbursement) electronically, their manager is notified and can approve or decline, and then the funds are released to that employee.

This way, you have the request and approval, the people who made each, the date, time, and reason for spending all in one place, with no email trail to worry about.

Transaction data

Perhaps the most important element of your audit trail is having your full payment history available on command. But that gets tricky when you have different, disconnected ways of paying for things.

If you have to look back through credit card statements, expense claims (and their receipts), invoices, and petty cash, you’re creating extra work just to compile the data. Instead, you want transaction data captured at the source, categorized and saved into one central repository.

This is why we always advocate for all-in-one spending platforms. If you can manage in-person card payments, virtual card payments, employee expense reimbursements and invoices from the same solution, you always know where to find transaction data.

Every transaction is automatically recorded and stored in an easy-to-find place, ready to hand over to auditors in one go.

Supporting documents

For many finance team members, it can feel like chasing teammates for receipts and invoices is half the job. And nobody signs up for that.

So one critical step in automating the audit trail is to give team members incentives to submit documents on time. The first step is to make tools available - a mobile app to snap pictures of receipts is a great option. So is a standard forwarding address for all their invoices. You want to keep the barriers as low as possible.

And you also need some ramifications for those who won’t follow the rules. For example, Spendesk’s Play by the Rules system blocks employees from spending if they have too many late or missing receipts. (It gives them plenty of warnings and chances to make it right, too.)

As we’ll see, if you’re relying on paper or email documents as evidence, you’re likely to find endless late or missing submissions. But if you let team members use the tools they know and love (like their phones), receipts come in on time and error-free.

A financial information hub

The vital characteristics of your data hub are that records exist and can be easily found. And the beauty of working with one central spending solution (as mentioned above) is that both will always be true.

First, for team members to spend, they have to follow every step in the process. They’ll be required to seek approval before spending, and reminded to upload receipts when they’re done.

And simply as a matter of course, everything is recorded in the system, with no extra work from finance. So you have the full audit trail waiting for you. No need to create special filing systems or copy everything in triplicate.

Essentially, you have a perfect audit trail without trying.

Automated audit trails: what's preventing you from making the switch today?

Let’s look at this from the other side. Suppose you stick with the expense processes you (and everyone else) have been using for decades. Can you automate with the tools you already have?

A few crucial (and painful) common business practices are keeping many companies trapped in the past.

Paper records

To automate effectively, you need to digitize. In practice, this means you simply can’t rely on paper receipts, invoices, expense claims, purchase orders, or any other paper records. These always need human intervention, either to file in huge cabinets or manually enter into digital records.

Digitized e-receipts are now accepted and encouraged by governments around the world. They’re obviously easier to store and harder to lose than paper, and they’re much faster to find in case of audit (if saved sensibly). And the same goes for invoices and expense claims.

Email approvals

When the average employee makes a large purchase using company money, they need managerial approval. And to track these approvals, many companies rely on an email chain that can then be printed or saved for later.

While this is “digital,” it’s still manual and slow. Emails need to be forwarded on to finance teams, and it’s common to have to wade back through months of communications to find them. Instead, you want approval workflows built into your purchasing systems. This way, approvals are recorded as a matter of everyday business.

Shared company cards

Among the litany of issues with the company credit card is the fact that they’re not actually designed to be shared. Companies everywhere do it, of course, but then have to follow up with emails and credit card statements to explain every purchase.

And then there are the security-conscious companies that don’t share cards around. Instead, they require the same office managers and finance team members to make every single purchase. This is tedious, frustrating work that also can’t be automated while relying on shared cards.

Audit preparation starts here

There’s a fun saying that applies to fitness, education, and really life in general:

“Stay ready so you don’t have to get ready”

That’s the basic ethos of this article. Why wait until an audit approaches to get your financial audit trail in place? This only creates a serious panic at the time when you can least afford one.

Instead, you can have spending processes that build the audit trail as you go. And without relying on you and your team to be extra diligent along the way.

In fact, smart spend management tools take the hard work off your shoulders, and keep you compliant as a simple matter of course. An automated audit trail is just one result of adopting these smart tools.

Learn how better spend management keeps you in total control of company spending and frees up your time and teams:

Curious how Spendesk works?

Try an interactive demo to see spend control and approvals end-to-end.

Get a free tour

)

)

)

)

)